Nigeria’s rising poverty is casting a shadow over the gains of the bold economic reforms embarked upon by President Bola Tinubu’s administration nearly two years ago, with experts calling for ‘targeted’ safety nets to cushion the pains of ordinary citizens.

While Tinubu’s government touts fiscal discipline, subsidy removal and a unified exchange rate as foundational steps toward long-term economic stability, surging poverty levels are overshadowing these policy wins.

A recent statement by the International Monetary Fund (IMF) revealed that while the government has taken important steps to stabilise the economy by abolishing costly fuel subsidies and liberalising its foreign exchange market, “gains have yet to benefit all Nigerians as poverty and food insecurity remain high.”

Read also: How Nigeria can lift its citizens off poverty — Peter Obi

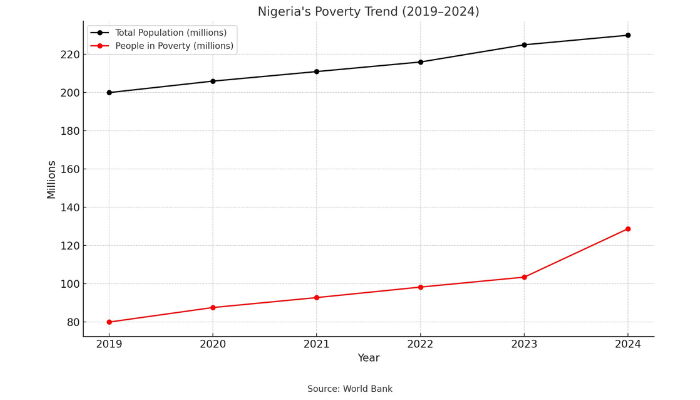

A joint report by the World Bank and the National Bureau of Statistics (NBS) estimates that over 129 million Nigerians—over half the population—now live below the national poverty line, a sharp increase from 104 million in 2023. Analysts attribute this jump to the combined effect of subsidy removal, inflation and job market stagnation.

Despite the government’s Renewed Hope Conditional Cash Transfer Scheme, aimed at reaching 15 million households with N75,000 each over three months, coverage and delivery issues have limited its impact. Civil society groups argue that palliative measures are “too little, too late” in the face of systemic hardship.

Akinwumi Adesina, president of the African Development Bank (AfDB), last week urged Nigeria to reduce poverty and improve the per capita incomes of citizens.

“Our GDP per capita in 1960 was $1,847. Today, it stands at $824. Nigerians are worse off than 64 years ago,” he stated.

He urged Nigerian leaders to end oil dependence and invest in technology, industry and innovation to build a resilient economy.

“Underdevelopment should not be accepted as our destiny. We must break free from this pattern,” he noted.

He said Nigeria can become an African industrial powerhouse, citing the Dangote Refinery as a transformative example.

Inflation surge, naira fall bite hard

Nigeria’s inflation rose for the most of 2024, averaging 33.2 percent as at the end of last year. But an overhaul of the consumer price index basket slashed inflation to 24.23 percent in March 2025 amid cost-of-living crisis.

Food inflation, a key pain point for households, also soared to nearly 40 percent last year, driven by rising transport costs, supply chain disruptions, and a weakened naira. The rebasing however put it at 21.8 percent last month.

The naira, on the other hand, has lost over 70 percent of its value since the mid-2023 when the FX unification policy began. The Central Bank of Nigeria (CBN) said the move was necessary to attract foreign investment and stabilise the market, but ordinary Nigerians have borne the brunt through skyrocketing prices of goods and services.

Read also: ‘Nigeria needs more rapid economic growth to lift its people out of poverty’

Though the naira has begun to stabilise following various reforms by the CBN, President Donald Trump’s recent ‘reciprocal tariffs’ has raised the risk of the currency reversing its gains, shedding about 5 percent of its value this month, despite hundreds of millions of dollars poured into the market to shore up the unit.

While the policy reforms by the government have been lauded both by local and international analysts, they have come with excruciating poverty on most Nigerians, which speaks to many of the structural problems that the country continues to face, according to Samuel Oyekanmi, research and insights associate at Abuja-based investment consultancy firm Norrenberger.

“In a bid to make these policy implementations have more grassroots effect, the government needs to prioritise targeted social safety nets, invest in human capital, drive an inclusive economic growth sector-wide and geography-wide, and finally ensure fiscal responsibility and transparency,” he said.

Private sector hit amid high jobless rate

The Manufacturers Association of Nigeria (MAN) said that over 300 manufacturing firms shut down or scaled back operations in the past year due to high energy costs and FX constraints.

Small businesses, which account for 84 percent of employment in Africa’s most populous nation, are grappling with reduced demand and unaffordable input prices.

Unemployment, which stood at 4.3 percent in the second quarter (Q2) of 2024 under a revised methodology, is projected by some private consultancies to be over 30 percent when underemployment and informal job losses are factored in.

President Tinubu has maintained that his reforms are essential to “save the economy from collapse.” His administration points to increased oil production, a rebound in FX reserves, and early signs of investment inflows as evidence that the economy is turning a corner.

However, economists warn that without targeted social protection, improved public service delivery and urgent investment in job creation, public support for the reforms may wane.

Nneka Eze, a development economist, said: “Structural reforms take time, but Nigeria doesn’t have the luxury of time when nearly half of its citizens are slipping into deeper poverty. The government needs a parallel strategy to stimulate the real economy while implementing fiscal discipline.”

What Nigeria must do to reduce poverty

According to Adesina, there are five priorities Nigeria must focus on: universal electricity, quality infrastructure, rapid industrialisation, innovation-driven growth, and competitive agriculture.

“The Nigeria of 2050 must be deliberately shaped — developed, corruption-free, and leading the rest of Africa,” he said.

Read also: Poverty is not a crime, embrace Pope Francis lifestyle, Akpabio tells Nigerians

Samuel Sule, chief executive officer of Renaissance Capital Africa, said Nigeria needs the reforms to ensure a balanced economy, stressing the importance of social protection for vulnerable people.

“A non-reversal of reforms while deliberately focusing on social protection, investment in infrastructure, government efficiency and a focus on economic stability (including reduced inflation) should have significant benefits in the medium term,” the Lagos-based investment bank chief said.